The OECD has just issued its half-yearly forecast for economic growth. It reckons that world real gross domestic product (GDP) will increase by just 3.1% this year and by 4% in 2014. Across the OECD countries, GDP is projected to rise by a meagre 1.2% this year and by 2.3% in 2014, while growth in non-OECD countries will rise by 5.5% this year and 6.2% in 2014. In the US, activity is projected to rise by 1.9% this year and by a further 2.8% in 2014. However, GDP in the euro area is expected to decline by 0.6% this year and then turn up just 1.1% in 2014, while in Japan GDP is expected to grow by 1.6% in 2013 and 1.4% in 2014.

These forecasts are more or less repeated by the IMF in its spring estimates. What stands out is that the mature capitalist economies are crawling along while the developing capitalist economies are growing at a reasonable lick. But the Eurozone area of 18 nations shows no sign of recovery from the Great Recession, with southern Europe deep in depression. The Euro leaders met last Monday and agreed that France, Spain, Greece etc could have more time to meet their fiscal targets on government budgets and debt because economic recovery was non-existent. So the pace of austerity was eased by the Euro leaders. But it’s still the message. As ECB President Mario Draghi recently maintained: “There was no alternative to fiscal consolidation, even though, we should not deny that this is contractionary in the short term. In the future there will be the so-called confidence channel, which will reactivate growth; but it’s not something that happens immediately”. Clearly not!

Christian Noyer, governor of the Bank of France, also echoed Draghi in saying that austerity was necessary to encourage the ‘confidence fairy’ to make an appearance: “Over a certain threshold, which our country has probably crossed, any increase in public spending and debt has extremely negative effects on confidence.” In other words, recovery is possible only if capitalists become confident that it will happen and that apparently depends on getting budget deficits and debt down. Why? Well, because “the old model doesn’t work any more”, namely traditional Keynesian efforts to boost demand by encouraging spending. Noyer added that France had to move away from public policies “overly concerned with preserving the jobs of the past” and allow for ‘liberalisation’ that could help future job creation.

And there we have it. As I have argued many times in this blog, the aim of austerity is not just to reduce public debt and government spending as such, but to restore the profitability of the capitalist sector. As Draghi puts it, “that’s why structural reforms are so important, because the short-term contraction will be succeeded by long-term sustainable growth only if these reforms are in place.” And that’s why when the Euro leaders relaxed the pace of austerity for several governments, they did so on the condition that ‘supply-side reform’ was stepped up, namely cuts in job security,wage levels and ‘protected’ industries along with more privatisation. That is the real aim of austerity: more neoliberal policies to restore the capitalist sector.

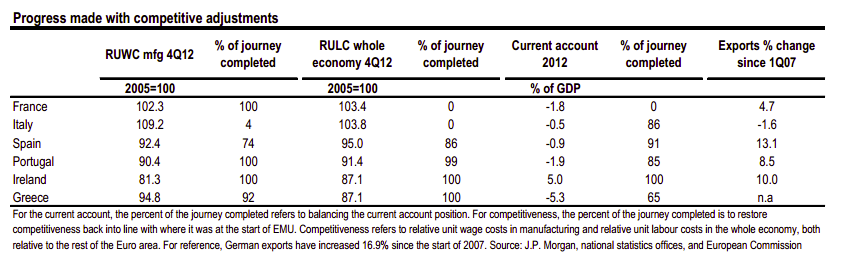

But is austerity working to achieve this? Well recently, JP Morgan economists put together some measures of progress: the amount of deleveraging achieved in public and private sector debt; more competitive prices for trade by the distressed states; making it easier to hire and fire employees; opening up ‘markets’, more privatisations and interestingly, progress on reducing democratic and constitutional obstacles in various states to imposing neoliberal policies.

JPM concluded that the Eurozone was only halfway there in this neoliberal recovery programme (The Euro area adjustment: about halfway there, 28 May 2013). For example, on the fiscal austerity targets, Italy was 75% on the way, Spain just 38%, Greece 97%, Ireland just 26% and Portugal 55%. Longer term austerity targets (meeting the Fiscal Compact in 2030) were more or less along the same distance.

Wage cuts and reductions in labour costs had gone further, with Ireland and Portugal having done enough, Greece a little further to go (after a 30% cut in living standards!) and Spain still another 25% to go.

But when it came to ‘structural reform’ i.e. reducing the size of the public sector, selling off state assets, reducing labour and pension rights, lower corporate taxes etc, progress had been much slower. Apparently, Italy, Greece, Spain and Portugal were still way less oriented to allowing the capitalist sector free rein than the likes of the Netherlands or Ireland.

JPM’s estimate of progress on the neoliberal programme is more realistic than the talk in financial markets that the likes of Greece or Ireland have ‘turned the corner’. Take Greece. The three parties in the coalition over the last year have stuck rigidly to the EU-IMF fiscal adjustment program. They have been awarded with an upgrade in the evaluation of Greek sovereign debt as a result by financial markets. Greece’s upgrade to B- comes almost a year to the day from the downgrade Greek sovereign debt to CCC, i.e. junk. So the ‘confidence fairy’ has shown itself from the undergrowth. But it is nowhere near enough to talk about the Greek crisis being over.

All the Euro bailout funds to Greece have gone on paying off Greece’s creditors, namely other European banks, pension funds and speculative hedge funds, the latter have made a killing as Greek debt interest rates have fallen as a result. But the real economy remains in a mess. The economy has had 19 consecutive quarters of contractions.

About 1.3 million Greeks are out of work, some 400,000 families have nobody earning an income, about 300,000 workers have employers who have not paid them for months and thousands have left the country to seek work, while the forces of neo-Nazism grow stronger. About 800,000 or so long-term unemployed have lost any access to benefits and free healthcare. Public services, such as health, have been ravaged, while the incessant rise in taxes has put terrible pressure on even the healthiest of businesses.

People in Greece worked 2,032 hours a year in 2011, considerably higher than the OECD average of 1,776 hours. By contrast, the Germans, clocked in on average 1,413 hours a year. Yet the average annual disposable household income in Greece is €15,800, way less than the OECD average of €17,820 a year. On indicators used of the OECD’s better life index, Greece ranks 30th out of 36 countries. In the EU, only crisis-ridden Slovenia ranks worse. Portugal came in at 28.

Small businesses in Greece are paying an interest rate of around 7% for credit assuming they can even get a loan from the country’s semi-comatose banking system. In contrast, similar firms in Germany borrow at half that rate. The current account deficit may have shrunk by about 7% pts of GDP but this been achieved largely on the back of a substantial fall in imports rather than a significant rise in exports. Even the dreaded Troika admitted in analysing the impact of its austerity programme that: “The rich and self-employed are simply not paying their fair share, which has forced an excessive reliance on across-the-board expenditure cuts and higher taxes on those earning a salary or a pension.”

Recovery in Greece depends on a return of investment in industry and key services. But there is little sign of that. In 2012 investment fell by 20% from the already ridiculously low levels of 2011. And the government is predicting a further fall in investment in 2013.

So if austerity is only half working at best to restore capitalism in the Eurozone, what is the alternative? Well, there is another that is gaining prominence, especially within the distressed Euro states like Portugal, Greece and Italy. It is the Keynesian alternative of leaving the euro and restoring a devalued national currency. For example, in Portugal, economist Joao Ferreira do Amaral has published a book urging Portugal to exit the euro. This has become a best seller and is backed not just by the Communist Party but also endorsed by the Supreme Court President! The book argues that austerity won’t work and the divergence between rich Germany and poor Portugal will only get wider if the current government’s policy is maintained. The only answer is to exit the Eurozone and for Portugal to restore its escudo as in the 1990s.

The claim of these ‘exit’ supporters is that the cost of exiting the euro to the economy will be much less than the continuing cost of austerity imposed by the Euro leaders on the likes of Portugal or Greece. These arguments are presented more theoretically by a new paper from Heiner Flassbeck and Costas Lapavitsas (Systemic_Crisis). Flassbeck is a former Vice Minister of Finance under left Social Democrat Oskar Lafontaine and seems to have formed an alliance with ostensible Marxist economist Lapavitsas to argue the case for exiting the euro as the only solution. In doing so, they seem to have arguments very similar to those of many neoliberals like Dr Werner Sinn, now a leader of the new ‘exit party’ in Germany that calls for a return to the mark. Lafontaine has also moved to this viewpoint. So there is an alliance between some nationalist neoliberals and Keynesians for an exit policy.

The problem that I have with this exit policy is that it is a bit like the position of the Irish Republican Army (IRA) on the issue of Irish unity. The IRA argued that first we must end ‘the border’ that divided north and south Ireland and then we can adopt socialist policies. Yet Ireland is still divided and still capitalist and the former leaders of the IRA now work within the existing two regimes for social change – a reversal of their old position. The euro exit is also a ‘two-stage’ theory: first, we must exit the euro as the top priority and then we can talk about socialist policies to end the crisis. I am sure that Lapavitsas and Amaral want to adopt policies for public ownership of the banks and major industrial sectors, public investment and a plan for Europe, but I think they obscure the battle against austerity by emphasising euro exit and devaluation as the major cure. Surely, this is a diversion.

Why? Well,as I said in a previous post

(http://thenextrecession.wordpress.com/2013/03/16/workers-punks-and-the-euro-crisis/), it is because the euro crisis is a crisis of capitalism and not a crisis of the euro. In other words, even if the euro were to collapse and EMU states returned to running their own monetary and currency policies, the crisis would not go away and may even get worse. That’s because the euro crisis is the product of the failure of the capitalist mode of production globally. It has had the worst impact on the weaker capitalist economists like Greece, Portugal or Slovenia, but it has hit all economies. The crisis is only partly a result of the policies of austerity being pursued, not only by the EU institutions, but also by states outside the Eurozone like the UK. If that is right, then alternative Keynesian policies of fiscal stimulus and/or devaluation where possible, will do little to end the slump and will still make households suffer income losses. Austerity means a loss of jobs and services and thus income. Keynesian policies also mean a loss of real income through higher prices, a falling currency and eventually rising interest rates.

Take Iceland, a country outside the EU, let alone the Eurozone. Devaluation, or Keynesian-style ‘beggar-thy-neighbour policies, have still meant a 40% decline in average real incomes in dollar terms and nearly 20% in krona terms since 2007 (see my post, http://thenextrecession.wordpress.com/2013/03/27/profitability-the-euro-crisis-and-icelandic-myths/). If not Iceland, then Argentina in 2001 is dug up as a successful ‘exit’ strategy. Argentina ended the peso’s peg with the dollar and devalued, apparently escaping its depression. But for Greece it is not just a question of breaking a peg with the euro. It will have to introduce a new drachma. Would this new currency issued by an effectively bankrupt state have any exchange value whatsoever? Will the Russians accept a Cypriot pound in exchange for oil, and the Americans drachma in exchange for medicines? Greece, which, unlike Argentina, is not a net exporter of raw materials with rising prices and so has little to support any new currency. Greeks can print as much as they like of it, but will they be able to buy electrical appliances, cars or even foods produced abroad with it?

And anyway, Argentina did not escape its crisis by breaking the peg with dollar. Guglielmo Carchedi and I are just about to publish a paper (The long roots of the present crisis: Keynesians, Austerians and Marx’s law) that will show that it was not competitive devaluation that restored Argentina’s growth after the 2001 crisis, but default on state debt caused by the previous destruction of productive capital. Argentina’s recovery was fuelled neither by devaluation nor by redistribution policies, but by the re-creation of previously destroyed private capital in the private sector with a low organic composition; a rising rate of exploitation; and improved efficiency. This is the cause—rather than Keynesian policies—of Argentina’s economic revival.

The euro project was unique in one way. It was designed to achieve integration and convergence among various European capitalist states but without establishing a full federal union of Europe, with one government, one budget, one set of tax laws and one banking system. For a while, it seemed to work until the crisis came, although even in the boom years, there was more divergence than convergence.

Can the euro’s halfway house now survive? It is clearly not going towards some federal union of European states, whatever the claims of the nationalist sceptics of UKIP or Front National. A united states of Europe under capitalism is not on the agenda. But the halfway house could lumber on if economic growth returns. But growth depends on investment. And investment has collapsed and not just in the weaker capitalist economies of the Eurozone.

The figure above is from Greek Default Watch (http://www.greekdefaultwatch.com/2013/05/the-eurozone-since-2007-in-one-image.html). The first column shows real GDP indexed at 100 in 2007. The Eurozone as a whole by 2012 remained below the level of 2007. And most Eurozone economies are still well below their 2007 levels – Greece is down 21%. The next columns show the changes in GDP since 2007 by expenditure sectors. The drop in GDP is really a factor of Germany growing (+€85 billion) but without a supporting cast to offset the declines in Italy (-€102 billion), Spain (-€40 billion) and Greece (€42 billion). On a net basis, Italy’s decline accounts for the bulk of the decline in the overall Eurozone, while Germany’s gain offsets the decline in Greece and Spain and the rest of the union is more or less even.

The Eurozone has a clear investment problem: investment rose in only one of the 17 countries (Luxembourg). The issue of external competitiveness that the Keynesian exit economists emphasise, just like the neoclassical neoliberals is less important. For the seven countries whose 2012 GDP was higher than in 2007, net exports made a big difference in only three cases; of the ten countries where GDP declined, net trade made a material contribution in seven, but this was not enough to offset the decline in investment. In other words, the problem for the weaker Euro capitalist states is not external competitiveness, but investment— it’s a very conventional capitalist crisis.

And as I have shown in previous posts, investment under capitalism depends on restoring profitability. Yet, with the exception of Ireland, all the peripheral EMU economies still have much lower rates of profit than their peaks before the global crisis of capitalism hit. With the exception of Italy, profitability did recover in 2012, while in the case of Ireland, profitability turned round as early as 2010.

It’s a halfway house. Austerity is working but very slowly. Last Monday, ECB Board member Jörg Asmussen denied that there is a “Euro Crisis”, though he admitted Europe has ‘a decade of “adjustments” ahead. Can the euro project survive another five or more years of austerity? Is it half full of success or half empty?

There is a third way out of the Eurozone’s crisis: a socialist option. That would involve Eurozone governments renegotiating and writing off public sector debt owed to the banks and other financial entities. To pay for the losses that the banks incur, rich bank share and bond holders would be liquidated and Europe’s big 30 banks would be taken into public ownership. They would become part of a Europe-wide New Deal to start public investment projects that could deliver jobs and housing and new technology. Governments would share Europe-wide revenues from each according to their abilities and to each according to their needs – as in a proper political and fiscal union based on common ownership and under a democratically endorsed plan for growth and welfare.

Of course, such a ‘Soviet Europe’ is not on the agenda and is thus utopian. But then exit from the Eurozone by ‘oppressed states’ is also not on the agenda of any government in the Eurozone or even in the main opposition parties. So it is equally ‘utopian’ with the added problem that it would not solve anything.

Leaders of Leftist parties like Syriza from Greece, IU from Spain, Front de Gauche in France etc have been meeting to discuss a joint programme for the Euro 2014 elections (http://www.publico.es/456053/la-izquierda-europea-se-pone-en-marcha-para-conquistar-bruselas). Will that programme adopt the vision I expressed above or not? If not, then we are faced with years (decade?) of more austerity.

There is a third way out of the Eurozone’s crisis: a socialist option. That would involve Eurozone governments renegotiating and writing off public sector debt owed to the banks and other financial entities. To pay for the losses that the banks incur, rich bank share and bond holders would be liquidated and Europe’s big 30 banks would be taken into public ownership. They would become part of a Europe-wide New Deal to start public investment projects that could deliver jobs and housing and new technology. Governments would share Europe-wide revenues from each according to their abilities and to each according to their needs – as in a proper political and fiscal union based on common ownership and under a democratically endorsed plan for growth and welfare.

Of course, such a ‘Soviet Europe’ is not on the agenda and is thus utopian. But then exit from the Eurozone by ‘oppressed states’ is also not on the agenda of any government in the Eurozone or even in the main opposition parties. So it is equally ‘utopian’ with the added problem that it would not solve anything.

Leaders of Leftist parties like Syriza from Greece, IU from Spain, Front de Gauche in France etc have been meeting to discuss a joint programme for the Euro 2014 elections (http://www.publico.es/456053/la-izquierda-europea-se-pone-en-marcha-para-conquistar-bruselas). Will that programme adopt the vision I expressed above or not? If not, then we are faced with years (decade?) of more austerity.

0 comments:

Post a Comment