Mick Brooks comments here on the debate within the Committee For a Workers' International on the causes of the Great Recession and capitalist crisis. Check out a review or order Mick Brooks' book here .

by Mick Brooks

Since the outbreak of the Great Recession Marxists have debated its cause. This is a vital theoretical issue for understanding the world around us.

The debate centres around the issue as to whether the present crisis is caused by falling profits as explained by Marx’s law of the tendential fall in the rate of profit (LTFRP), dealt with in chapters 13-15 of ‘Capital Volume III’. Others argue that the crisis can be explained as one of underconsumption.

This debate is bubbling under within the ranks of the CWI. The leadership of the CWI (as of the IMT) take what I would characterise as an underconsumptionist position. Already two blogs are circulating inside the ranks of the CWI that advocate the LTFRP explanation, in addition to an excellent short film, and debates are beginning to take place in the localities. Signs of intelligent life? It looks like it. Check out:

Marx returns from the Grave, http://69.195.124.91/~brucieba/

Socialism is Crucial, http://socialismiscrucial.wordpress.com/

It should be explained at the outset that all parties agree that a crisis of capitalism takes the form of overproduction, of unsold goods, as it says in the ‘Communist Manifesto’. Overproduction and crisis, however, are not permanent features of capitalist production. It remains to be explained why capitalism dips into crisis when it does.

The leadership, reacting to criticism, has resorted to an ‘underconsumptionist’ explanation of the cause of crisis. The crisis is caused, according to a quote from Chapter 30 of ‘Capital Volume III’ by “the poverty and restricted consumption of the masses.” (As one of the bloggers, CrucialSteve, points out this was actually a bracketed note added by Engels into the original text.)

The problem with the underconsumptionist explanation is that there is a permanent tendency for capitalism to restrict the purchasing power of the working class, because it is a system based on profit. Underconsumptionism therefore has no explanatory power as an explanation of crisis.

In any case not all commodities are produced for workers – pallet trucks and computer numerically controlled machine tools are capital goods bought by capitalists. There are also luxury goods consumed only by capitalists such as yachts and private jets. Why should there be a specific outbreak of overproduction of consumer goods intended for workers’ consumption such as jumpers rather than pallet trucks or yachts? Empirically crises of overproduction usually break out in the capital goods industries. Investment is the most volatile element in national income.

The opposition bloggers within the CWI have a powerful argument in their favour – the rate and mass of profit in the major capitalist countries fell sharply prior to the onset of crisis in 2007. Marx’s theory is confirmed! To take the case of the USA:

“The US Bureau of Economic Analysis (BEA) shows that in the 3rd quarter of 2006 the mass of profits peaked at $1,865bn. By the 4th quarter of 2008 it bottomed out at $861bn.” (Brooks – Capitalist crisis; theory and practice, p.32)

The facts confirm Marx’s analysis of the LTFRP as the fundamental cause of crisis. Why should this cause surprise, since we all agree that capitalism is a system of production of profit?

The school of Marxian economists who support this analysis view the falling rate and also mass of profit only as an underlyingcause of crisis. Essentially the argument is about levels of causation in the crisis. What about the financial aspect of the crisis – the housing bubble, crazy loans and collapsing banks? Of course this was all very important. These specific factors profoundly influence the depth and nature of the downturn. Every crisis is a unique event with its own characteristics. But, with or without a ‘financial crisis’ the fact that the mass of profits in the USA, the most important capitalist country, halved over two years would have provoked a big collapse of output in any case.

How does the leadership of the CWI deal with the detailed criticisms of their approach thrown up by the advocates of the importance of the LTFRP as an explanation of crisis? Lynn Walsh argues in ‘Socialism Today’ that profit and investment have become disconnected in recent decades. “Despite the staggering increase in the share of income taken by the top 1% in the US, investment declined.”(‘Socialism Today’, November 2012) So profits (with the share of the top 1% as a proxy) are supposed have soared at the expense of working people, but this has not translated into productive investment. Walsh concludes, “This factual data..., in our view confirms the analysis of a crisis in capital accumulation put forward in ‘Socialism Today’ over many years” (ibid.).

If true, this is not an explanation for a pattern of booms and slumps. It presents a stagnationist perspective for the future of capitalism, a permanent slowing down of the rate of accumulation. Is the CWI serious about decades of stagnation? How do they explain the present crisis, where investment fell as a result of the fall in profits?

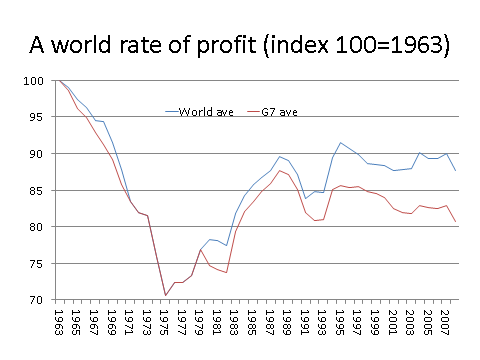

In fact there is a simple explanation for this alleged disjunction between profits and investment: the profit figures quoted are wrong. Michael Roberts has meticulously chronicled the rate of profit since the Second World War in his blog. Nobody has challenged his figures, which attempt to look beneath conventional statistics to work out a Marxian rate of profit.

Roberts concludes: first that there has been no return to the fabulous profits enjoyed by capitalists during the golden years of the post-War boom; and secondly that the rate of profit today in 2013 remains below that of 2007 before the onset of the great Recession. Andrew Kliman also carefully shows (in ‘The failure of capitalist production’) that the reason for lower investment in the years since 1974 is lower profits. There is just less to invest. Simples.

The CWI leadership buttress their ‘explanation’ as to why investment has been lower with recourse to the notion of financialisation. As Lynn Walsh argues in the same article, more and more funds have been gobbled up by financial shenanigans in preference to investing in industry. There is no mystery here. In so far as more “profits disappeared into the financial sector” (ibid.), that is a response to lower pickings to be made in production – because of the LTFRP itself.

Increasing exploitation of the workers over recent decades has not led to increasing rates of accumulation because of financialisation, it is asserted. This is part of the analysis of a whole school of thought, regarding itself as Marxian, which sees the current crisis as one of the neoliberal form of capitalism rather than capitalism as a whole. In fact this is the conventional wisdom of the majority of academic Marxist economists. A whole new stage of capitalism is supposed to have developed since about 1980, buttressed by the holy trinity of globalisation, neoliberalism and financialisation.

Dumenil and Levy’s book – ‘The crisis of neoliberalism’, 2011 – is an example. Phil Hearse writing in Socialist Resistance, the publishing house of the so-called Fourth international, also refers to “a neoliberal ‘regime of accumulation’”. The logic of this approach seems to be that neoliberalism should be destroyed rather the capitalist system overthrown.

As we see, the CWI leadership has swallowed this analysis whole. By accepting the interpretation of this school the CWI is on a slippery slope indeed. We’re with the opposition within their ranks on this one.