In my view, we are now in a Long Depression, centred in the advanced capitalist economies but also affecting the emerging capitalist economies. The latter do better because they still have ample supplies of cheap labour available to exploit (well, at least some larger emerging economies do). So absolute surplus value can be increased without Marx’s law of profitability applying too strongly. What do I mean by that?

Well, capitalists are permanently engaged in the search for value, or more specifically, surplus value. They can get that globally by drawing more of the population into capitalist production. The big issue is how much longer capitalism can continue to appropriate value from human labour power when the workforce globally can no longer expand sufficiently.

Ironically, the UK’s right-wing City paper City Am put it from the perspective of capital: “People, not commodities, land or even capital, are the ultimate resource of an economy, as the US academic Julian Simon famously put it. Without talented, motivated, skilled and educated individuals, nothing is possible; capital itself is a product of labour. Human ingenuity is able to overcome everything. Malthusians who dream of a shrinking population and who reflexively believe that every country is over-populated are wrong. This is always a lesson that nations suffering from shrinking populations relearn at great cost: all the productivity growth in the world is rarely enough to compensate for the psychological and actual effect of a declining population.”

More important, more people means more potential value to be appropriated by capital. But getting more value and surplus value through extending the size of the workforce is increasingly difficult or even impossible in many advanced capitalist economies.

Instead, in these economies, capitalists must try and raise surplus value though the intensity of work and through more mechanisation and technology that saves labour i.e relative surplus value. But that, as Marx explained, brings into operation the law of the tendency of the rate of profit to fall and the ultimate barrier to further accumulation and growth in value (see my post on http://thenextrecession.wordpress.com/2012/09/12/crisis-or-breakdown/).

Indeed the crisis in the south of the Eurozone is creating permanent damage to these economies: it is not just that their GDPs are shrinking, but there is an exodus of the workforce. The number of Greek and Spanish residents moving to other EU countries has doubled since 2007, reaching 39,000 and 72,000 respectively in 2011, according to new figures on immigration published by the OECD. In contrast, Germany saw a 73% cent increase in Greek immigrants between 2011 and 2012, almost 50% for Spanish and Portuguese and 35% for Italians.

Japan is also suffering from the lack of expansion of its workforce. In the short term GDP per capita growth in Japan looks better than its GDP growth so that US GDP per capita growth in recent years is little better than Japan. Indeed on a per capita basis, the US has been stagnant since 2008 and Japan has risen slightly.

But longer term, this is bad news for Japan as its debt burden will mount and its working population to dependents will decline. This is a growth and debt time bomb. The move to crisis may be slow because Japan has huge reserves of FX reserves and foreign assets built up over decades so it has lots of funds to fall back on. Japan’s net international investment position is 56% in the positive while the US is 19% in the negative. Also its debt is mostly owned by its own citizens (only 7% by foreigners) while US government debt is 40% owned by foreigners. However, the US dollar is still the world’s reserve currency, giving the US considerable leeway in funding its deficits and debt. Japan’s banks and government are so intertwined that they will both go down together. In the 1990s, the banks were bailed out by government; currently the banks are bailing out the government. Next time, they both go down together.

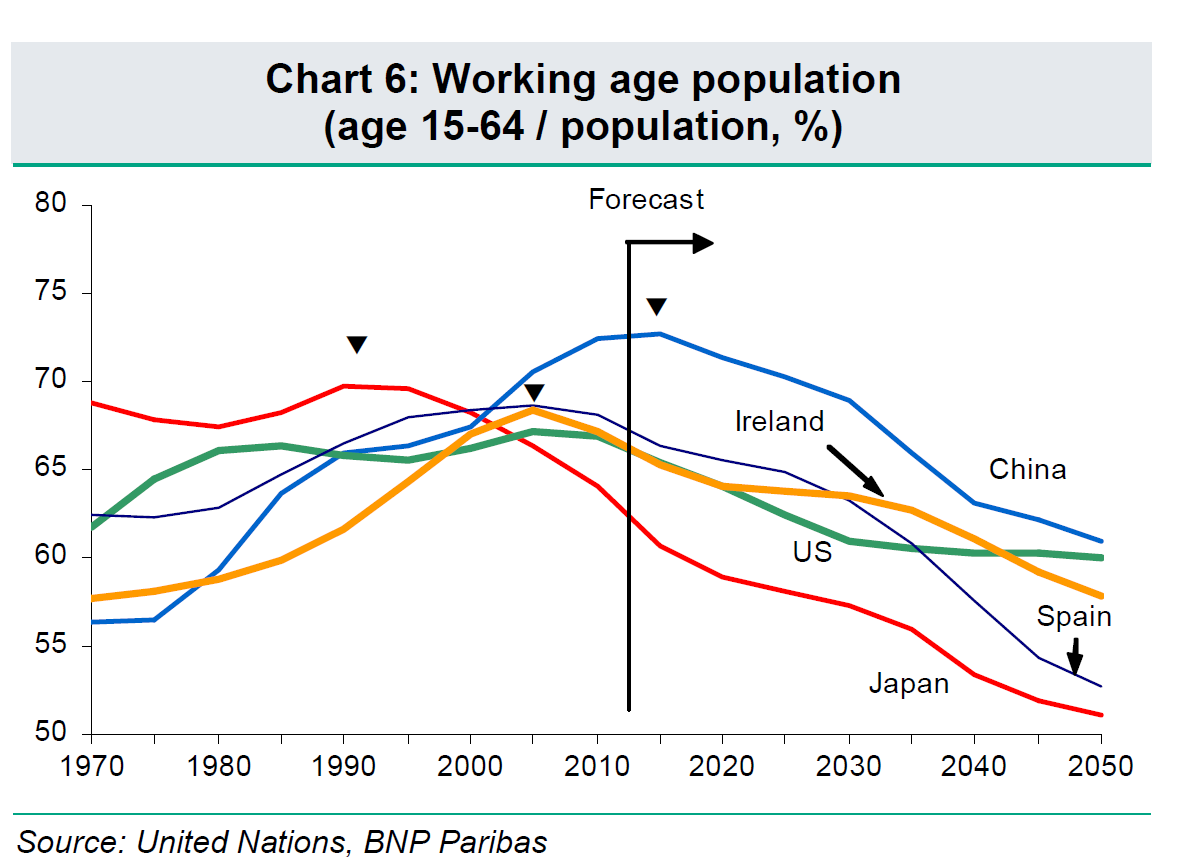

George Magnus (Economic insights by George Magnus, 19 June, Demographics: from dividend to drag) recently pointed out that the support ratio in the US and Europe in the early 2000s was similar to that of Japan ten years earlier. It shows that from about 2016, the decline in China’s support ratio starts to speed up, so that by 2050, it will have fewer workers per older citizen than the US. It also includes India, by way of comparison, as the representative of the bulk of emerging markets and developing countries. India’s support ratio is predicted to grind lower but even by 2050, it will still be only the same as that in Western countries in the 1990s. From the 1960s onwards – a little earlier in Japan – the total support ratio rose everywhere and more or less continuously, until about 1990 in Japan, and 2005-2010 in the US and Europe. Japan’s support ratio is now approaching 1.5 workers per older citizen, and is predicted to carry on falling to parity in the middle of the century. The US and Europe are predicted to follow Japan, though support ratios are not expected to fall as far.

China and other emerging economies have not yet reached the point where the working population is no longer rising and the expansion of absolute surplus value is restricted – the so-called Lewis turning point (see my post, http://thenextrecession.wordpress.com/2012/11/16/chinas-transition-new-leaders-old-policies/). But China is not far away. In the meantime, China is pushing ahead with a sweeping plan to move 250 million rural residents into newly constructed towns and cities over the next dozen years — a massive of expansion of labour power into production. The broad trend began decades ago. In the early 1980s, about 80% of Chinese lived in the countryside but only 47% today, plus an additional 17% that works in cities but is classified as rural.

And there are still huge reserves of labour as yet untapped, particularly in Africa. The latest UN population projections for the world’s economies show that Africa is expected to dominate population growth over the next 90 years as populations in many of the world’s developed economies and China shrink. Africa’s population is expected to more than quadruple over just 90 years, while Asia will continue to grow, but peak about 50 years from now then start declining. Europe will continue to shrink. South America’s population will rise until about 2050, at which point it will begin its own gradual population decline. North America will continue to grow at a slow, sustainable rate, surpassing South America’s overall population around 2070.

George Magnus (Economic insights by George Magnus, 19 June, Demographics: from dividend to drag) recently pointed out that the support ratio in the US and Europe in the early 2000s was similar to that of Japan ten years earlier. It shows that from about 2016, the decline in China’s support ratio starts to speed up, so that by 2050, it will have fewer workers per older citizen than the US. It also includes India, by way of comparison, as the representative of the bulk of emerging markets and developing countries. India’s support ratio is predicted to grind lower but even by 2050, it will still be only the same as that in Western countries in the 1990s. From the 1960s onwards – a little earlier in Japan – the total support ratio rose everywhere and more or less continuously, until about 1990 in Japan, and 2005-2010 in the US and Europe. Japan’s support ratio is now approaching 1.5 workers per older citizen, and is predicted to carry on falling to parity in the middle of the century. The US and Europe are predicted to follow Japan, though support ratios are not expected to fall as far.

China and other emerging economies have not yet reached the point where the working population is no longer rising and the expansion of absolute surplus value is restricted – the so-called Lewis turning point (see my post, http://thenextrecession.wordpress.com/2012/11/16/chinas-transition-new-leaders-old-policies/). But China is not far away. In the meantime, China is pushing ahead with a sweeping plan to move 250 million rural residents into newly constructed towns and cities over the next dozen years — a massive of expansion of labour power into production. The broad trend began decades ago. In the early 1980s, about 80% of Chinese lived in the countryside but only 47% today, plus an additional 17% that works in cities but is classified as rural.

And there are still huge reserves of labour as yet untapped, particularly in Africa. The latest UN population projections for the world’s economies show that Africa is expected to dominate population growth over the next 90 years as populations in many of the world’s developed economies and China shrink. Africa’s population is expected to more than quadruple over just 90 years, while Asia will continue to grow, but peak about 50 years from now then start declining. Europe will continue to shrink. South America’s population will rise until about 2050, at which point it will begin its own gradual population decline. North America will continue to grow at a slow, sustainable rate, surpassing South America’s overall population around 2070.

China’s population is soon expected to go into decline , whereas India’s is expected to grow strongly for another 50 years, and the US’ and Indonesia’s populations are projected to grow steadily. Nigeria’s population is expected to explode eight-fold this century.

0 comments:

Post a Comment