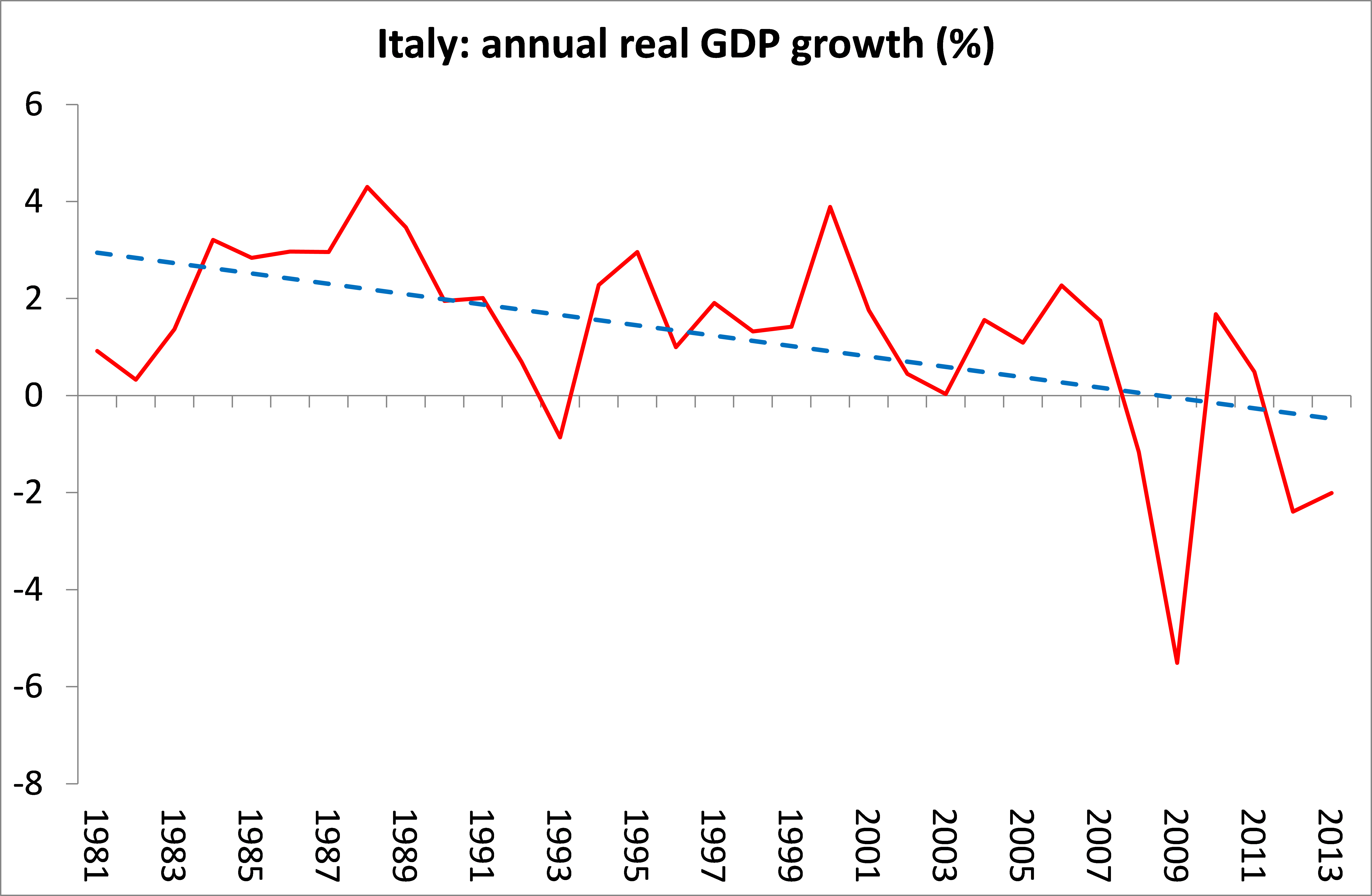

We hear all the time how this the US is greatest country in the world and all that. Of course, every ruling class says this in its efforts to create national pride and convince the masses that nowhere can equal the treatment their particular government affords. Most American's mind you are well aware that here in the US if you have no money "you're on your own baby". We're told waster like George W Bush or the hedge fund managers, bankers and other coupon clippers all pulled themselves up by their own bootstraps which of course is nonsense. The social services in the US, a 24 hour consumer society are extremely poor as the individual is supposed to fend for themselves. that's how it works. But we are in the greatest society on earth. The unelected rulers of the US wouldn't care at all if the US working class never traveled anywhere. They'd prefer we know nothing other than what we see on their TV. We thought our readers might find this piece of interest about how another society, Finland, deals with the question of pregnancy and childbirth. It is from the website, Mothering.

The Finnish Baby Box

by Christine Gross-Loh, author of the new book Parenting Without Borders: Surprising Lessons Parents Around the World Can Teach Us

I’ve long been fascinated by motherhood around the world. What is it like to birth in another country? What’s the lore on starting solids in another culture? How do children play in other countries? How do they sleep and who sleeps with them? How do cultural or societal supports ease the transition to new parenthood?

But it was worth it. Hilla begins each day by kicking off her baby box bedding and exclaiming “boof!” At seven months, she’s outgrown the pajamas, still wears much of the box’s other clothing, and has yet to grow into a good deal more. There’s no sign of teeth in her gummy smile, so the toothbrush has gone unused. The teething ring and rhyme book, however, are part of an important morning ritual of toy and book mayhem. If we take the stroller out, Hilla will get bundled into the baby box snowsuit and sleeping bag–cleverly sized items that might just last until next winter if we’re lucky. Then there are the breast pads for mother, the bib for a messy little mouth experimenting with solids, and the towel that dries chubby baby bodies after the narrative of the day’s events has been washed away. Hilla is tucked into her duvet until morning, when baby legs decide it’s time to start a new day.

I’ve long been fascinated by motherhood around the world. What is it like to birth in another country? What’s the lore on starting solids in another culture? How do children play in other countries? How do they sleep and who sleeps with them? How do cultural or societal supports ease the transition to new parenthood?

My friend Michele, an American new mother living in Finland, joins me here today to help satisfy my curiosity about motherhood abroad, in her guest post below.

The Finnish Baby Box

by Michele Simeon

In Finland, spotting babies with the same birth year isn’t just a matter of judging size. A famed national health care benefit of my adopted homeland is the maternity package, known as the ‘baby box’ in our household. Expecting mothers receive a large, cardboard box, itself designed to act as the baby’s first bed, full of gender neutral infant clothing and other essentials. Those who would prefer to purchase their own supplies instead receive a grant, and mothers carrying more than one child receive increased benefits on a graduated scale, so that e.g. families with twins can receive any combination of three grants or boxes.

The baby box is unique in the world and has been available in Finland to low-income mothers since 1937 and to all mothers since 1949. Each year, the designs and colors vary, creating allegiances of palettes and nostalgia for those special colors of infancy. You can view an inventory of the 2010 box here.

I pounced on my daughter Hilla’s baby box like it was the biggest, best Christmas present I’d ever received–that is, after hauling it uphill during a heat wave, eight months of pregnant belly weighing me down, much to the dismay of passersby. ‘It’s big and heavy,’ the kind postal worker had warned me. ‘That’s OK’ I beamed enthusiastically before realizing that my protruding middle prevented a conventional front carry.

But it was worth it. Hilla begins each day by kicking off her baby box bedding and exclaiming “boof!” At seven months, she’s outgrown the pajamas, still wears much of the box’s other clothing, and has yet to grow into a good deal more. There’s no sign of teeth in her gummy smile, so the toothbrush has gone unused. The teething ring and rhyme book, however, are part of an important morning ritual of toy and book mayhem. If we take the stroller out, Hilla will get bundled into the baby box snowsuit and sleeping bag–cleverly sized items that might just last until next winter if we’re lucky. Then there are the breast pads for mother, the bib for a messy little mouth experimenting with solids, and the towel that dries chubby baby bodies after the narrative of the day’s events has been washed away. Hilla is tucked into her duvet until morning, when baby legs decide it’s time to start a new day.

While the box alone cannot create material equality for all babies born in this country, it is only one of many benefits designed to give children a good, fair start to life. There’s no shame in using public aid that everyone accesses and there’s no statement of consumerist individuality in the clothing that all babies are wearing. The box gives us lots of fun opportunities to play baby punch buggy and it spared us more than a few shopping trips and plenty of money, but its real value lies in its message of social justice for all children.

What public benefits are available to families in your communities? Which would you like to see?

Image credit top: Finnish Baby Box by Roxeteer

Image bottom: Two-month-old Hilla naps in her baby box outerwear. The bear & bee duvet plus cover were also a part of the package.

Michele Simeon is an American writer and editor living in Helsinki. Visit her blog A House Called Nut where she writes about living abroad in Finland and her experience of multicultural, bilingual family life.

Christine is a mother of four, crafter, journalist, and author. She wrote The Diaper-Free Baby (HarperCollins, 2007), a book about elimination communication, and a book and craft kit, Origami Suncatchers (Sterling, 2011). She’s now writing a book about global parenting practices to be published by Avery, a Penguin Books imprint, in 2013. Visit her at her blog.