As I have said in a previous post (see http://thenextrecession.wordpress.com/2013/03/16/workers-punks-and-the-euro-crisis/), Slovenia is likely to be the next Eurozone state that will require a bailout after Cyprus. Slovenia’s banks need €1bn for recapitalisation after taking heavy losses on the commercial property development bust and on falling government debt prices (Italy?). And the new centre-left coalition needs about €3bn to cover the budget deficit and debt repayments this year. It does not look like it can find this money from the country’s own taxpayers and banks. So watch this space.

As Cyprus enters a long period of austerity with the banking sector decimated and the economy diving (one forecast is for a 20% fall in real GDP through to 2017), the debate continues. Is it better for small economies like Cyprus, Slovenia and even Greece to leave the Eurozone, institute their own currencies and devalue against the euro and the dollar, so they can grow through cheaper exports in world markets? Or is better to continue with the grinding down of living standards under the ‘heel’ of the dreaded Troika? Does leaving the euro mean that people can avoid a huge loss in jobs, public services and living standards?

My view is that either way, staying in or leaving the euro, will deliver more or less the same result for the majority. That’s because this crisis is not a crisis of the euro as such but a crisis of the capitalist mode of production. The way out for for the Eurozone is for austerity to lower the cost of production in the weaker states to the point where profitability begins to rise and these smaller economies can start to restore economic growth. The problem with this solution is that this could take a decade (it’s taken years already) and so it may never happen before capitalism enters another global slump – indeed, that may happen precisely because profitability cannot be restored.

There is some progress through austerity within the eurozone. A key proxy for competitiveness is an economy’s current account, the broadest measure of trade with the rest of the world. It shows improvement across the periphery EMU nations. The combined account of Greece, Ireland, Italy, Portugal and Spain narrowed to a deficit of 0.6 percent of gross domestic product at the end of last year from 7 percent in 2008 and will be in balance later this year. While a slide in imports accounts for some of the correction, Greece boosted its exports outside the EU by about 30 percent in the fourth quarter of 2012 from the previous year, while Italy’s rose 13 percent in January from a year ago. While austerity weakens consumer demand, it can begin to turn round profitability. For example, Spain has slashed social-security payments from companies, raised the retirement age and made it easier to fire workers. Portugal has weakened collective bargaining, cut redundancy payments and suspended four national holidays. Greece has pared public-sector wages, lowered the minimum wage, and eased redundancy rules; and is selling state assets.

A November study by Berenberg, a Brussels-based research group, found unit labor costs fell 10.5 percent from 2009 to 2012 in Greece, 10.3 percent in Ireland, 6 percent in Spain and 6.1 percent in Portugal. Over the entire euro-area they gained 1.5 percent. Relative labour costs in Spain and Portugal have now dropped below Germany’s for the first time since 2005. This has all helped to raise profitability in 2012 in most ‘austerity’ EMU economies (see graph). But, with the exception of Ireland, all the peripheral EMU economies still have much lower rates of profit than their peaks before the global crisis of capitalism hit. However, with the exception of Italy, profitability did recover in 2012. In the case of Ireland, profitability turned round as early as 2010.

Why has Ireland done relatively better? I think there are two reasons. First reducing unit labour costs in production has a much bigger effect on growth and profits in an economy like Ireland with annual exports equivalent to 100% of GDP compared to 20-40% in the other countries. Second, unit labour costs were cut so much more easily because of emigration. Irish youth, especially skilled workers, just left the country for the UK and elsewhere. Indeed, the turnaround from net immigration (or Irish returning home to a fast-growing ‘Celtic tiger’ before the crisis) to net emigration is truly dramatic.

Now many Keynesians like Paul Krugman or George Stiglitz argue that the euro crisis is a crisis of the failed project of the euro, not a crisis of capitalism. So the answer is for the smaller EMU states to leave the euro. For example, Krugman reckons the answer for the Cypriot people is to leave the euro. “Cyprus should leave the euro. Now. The reason is straightforward: staying in the euro means an incredibly severe depression, which will last for many years while Cyprus tries to build a new export sector. Leaving the euro, and letting the new currency fall sharply, would greatly accelerate that rebuilding… What’s the path forward? Cyprus needs to have a tourist boom, plus a rapid growth of other exports — my guess would be agriculture as a driver, although I don’t know much about it. The obvious way to get there is through a large devaluation” (http://krugman.blogs.nytimes.com/2013/03/26/cyprus-seriously/). Keynesians bemoan the fact that this advice has not been heeded.

But there is a good reason for this.

Take the example of Iceland. This tiny island, smaller in population that Cyprus, is not in the eurozone, or even the EU. But it is used as the model by many Keynesians (see Krugman on Iceland: http://krugman.blogs.nytimes.com/2012/07/08/the-times-does-iceland/) for Keynesian-style alternative policies, including devaluation. Krugman argues for “the relevance of the Icelandic sort-of miracle… What it demonstrated was the usefulness of devaluation (and therefore of having your own currency), and the case for temporary capital controls in an emergency. Also the case for letting creditors of private banks gone wild eat the losses. Iceland did not engage in fiscal stimulus; it didn’t have to, given the kick from a huge depreciation of the currency. And more broadly, Iceland is a dramatic demonstration of the wrongness of conventional wisdom in these times. .. Iceland broke all the rules, and things are not too bad.“

But did Iceland ‘break all the rules’ and are ‘things now not too bad’? This is another Icelandic myth according one Icelandic blogger: “people continue to spread the factually dubious statement that Iceland told creditors & IMF to go jump, nationalised banks, arrested the fraudsters, gave debt relief and is now growing very strongly, thanks. No, Iceland did not tell the IMF to go away (https://www.imf.org/external/country/ISL/). Iceland didn’t bail out the collapsed banks, but that wasn’t for the want of trying. If you read through the Report of the Special Investigation Commission you’d find out that the Icelandic government tried everything it could to save the banks, including asking for insane loans to pay off the banks’ debts (http://sic.althingi.is/). The short version is that they tried to save the banks, save the creditors and screwed up completely. Iceland arrested a few bank fraudsters, but just the pawns, small fry, and the lackeys.

Yes, Iceland did nationalise its banks but then privatised them again in record time. Two out of the three collapsed major banks in Iceland are now owned by their creditors, not the state. The third bank, Landsbanki, is still nationalised but that’s solely because of ongoing court cases involving Icesave. Most of the creditors actually sold their stakes onto foreign hedge funds. Some of the bankrupt banks only remained in government control for a few weeks. SPRON, for example, was merged into Arion Bank which in turn was given to its creditors a few weeks later. essentially a free gift to Kaupthing’s foreign creditors.

Iceland’s lauded recovery model involving devaluation of its currency coupled with capital controls is now a drag on growth. Iceland is growing at 2 percent, faster than much of Europe. But the IMF had originally forecast annual growth of around 4.5 percent from 2011-2013. It now is under half that. Many Icelanders say they do not ‘feel’ this modest growth. Outside booming fishing and tourism, businesses complain of stagnation. Some 80 percent of households are swamped in housing loan debts indexed to inflation. Investment is under 15 percent of GDP, a record low. State workers like nurses are raising worries about inflation amid increasing demands for better salaries. An hour’s drive from the capital to the town of Keflavik, dozens of Icelanders line up for free food aid. People must present rent or mortgage slips and their salary slips. Real incomes have dropped sharply for Icelandic households and their debt is index-linked to inflation. Pre-tax gross income of the average Icelander has decreased by 18.3% since 2007. Measured in USD however, the fall is 42.7% since 2007.

So both austerity and Keynesian-style devaluation have resulted in a sharp fall in living standards, whether in Greece or Iceland.

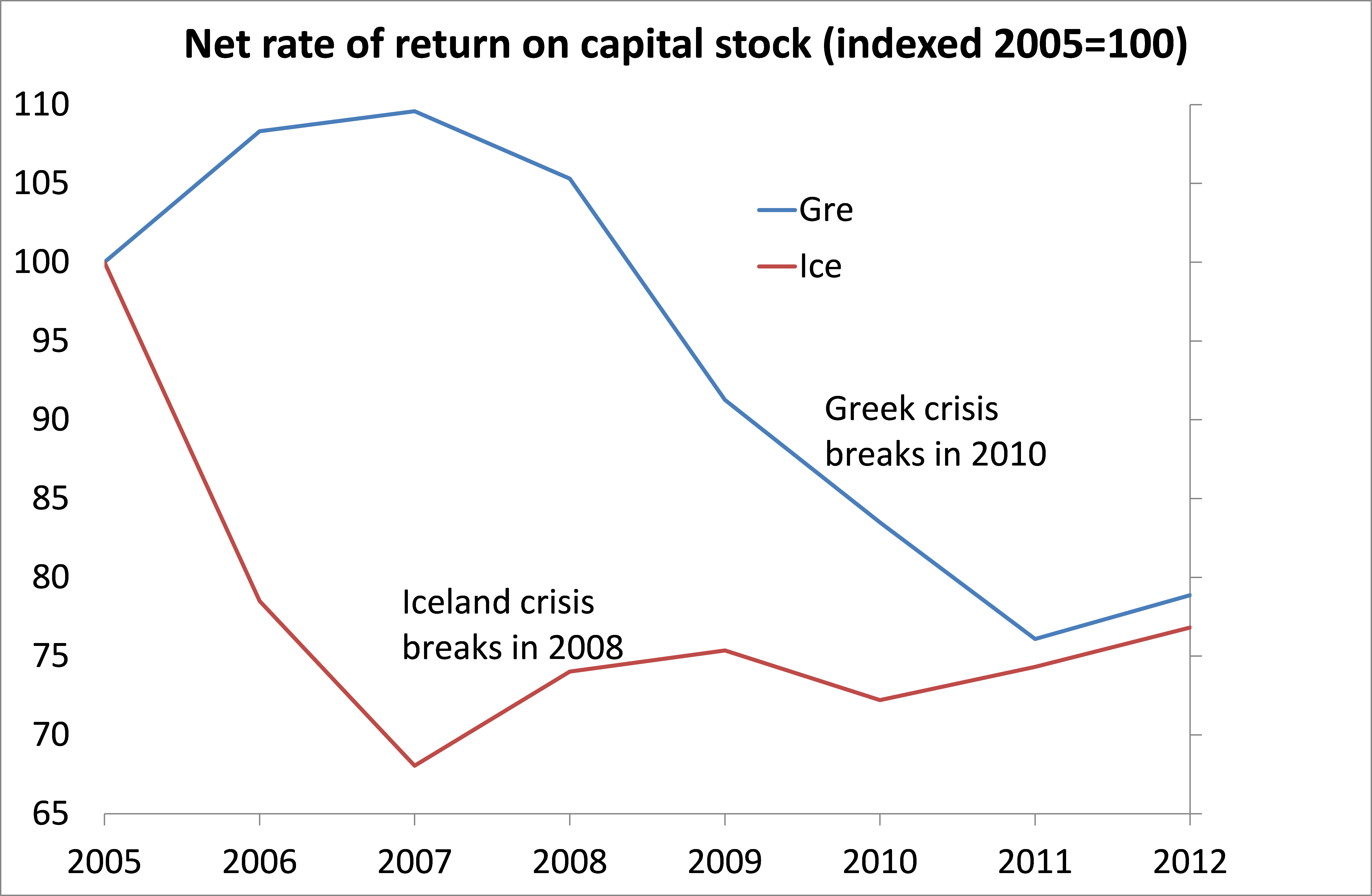

Restoring profitability is key for economic recovery under the capitalist mode of production. So which pro-capitalist policy has done best on this criterion? Let’s compare Greece and Iceland. Iceland’s rate of profit plummeted from 2005 and eventually the island’s property boom burst and along with it the banks collapsed in 2008-9. Devaluation of the currency started in 2008, but profitability in 2012 remains well under the peak level of 2004, although there has been a slow recovery in profitability from 2008 onwards. Greece’s profitability stayed up until the global crisis took hold and then it plummeted and only stopped falling last year. Profitability in ‘austerity’ Greece and ‘devaluing’ Iceland is now about the same relative to 2005 levels. So you could say that either policy has been equally useless.

Perhaps the biggest lesson of this crisis of capitalism is the lasting damage that the Great Recession and the subsequent Long Depression has had on the ability of the capitalist mode of production to deliver on profitability and economic growth. A recent study found that there has been a significant deterioration in long-term real GDP growth (http://www.voxeu.org/article/eurozone-looking-growth). Trend growth for the four main Eurozone countries is forecast to be a little less than 1% and slightly less than 2% after 2014, with trend growth highest in Spain and France; and the lowest for Italy and Germany.

Weak trend growth in a central scenario

Source: BofAML Global Research.

It could be even worse, if investment fails to recover quickly. Trend growth might well remain negative in Spain and Italy and may fail to increase for Germany or France. As the authors conclude, “this exercise shows the damage will indeed be long lasting, permanently impairing growth in a context of an ageing population that needs higher growth capacity than ever before.”

0 comments:

Post a Comment